Spot butadiene prices in May 2025 showed a staggering 44% gap between the US Gulf and China—USD 956 per ton versus USD 1,380 per ton. For manufacturers dependent on merchant feedstock, that volatility translates directly into unpredictable margins and supply disruptions. As raw-material swings intensify and global logistics remain fragile in 2026, leading nitrile producers are turning to vertical integration as their primary defense strategy. By controlling more steps in the value chain—from monomer procurement through nitrile rubber compounding and downstream manufacturing—companies are insulating themselves from external shocks while securing long-term cost advantages and supply continuity.

Vertical NBR Integration in Nitrile Production: How It Lowers Costs and Boosts Supply Stability has emerged as a critical competitive differentiator in the post-COVID era, when supply chains fractured and feedstock markets became increasingly unpredictable. This article examines how manufacturers are implementing integration strategies, the measurable impact on pricing volatility, and what industry analysts predict for market stability through 2033.

Key Takeaways

- Vertical integration reduces exposure to raw-material price swings, with butadiene and acrylonitrile costs varying up to 44% across regions in 2025.

- Integrated producers control quality, logistics, and supply continuity, making them better positioned to secure long-term contracts and weather trade disruptions.

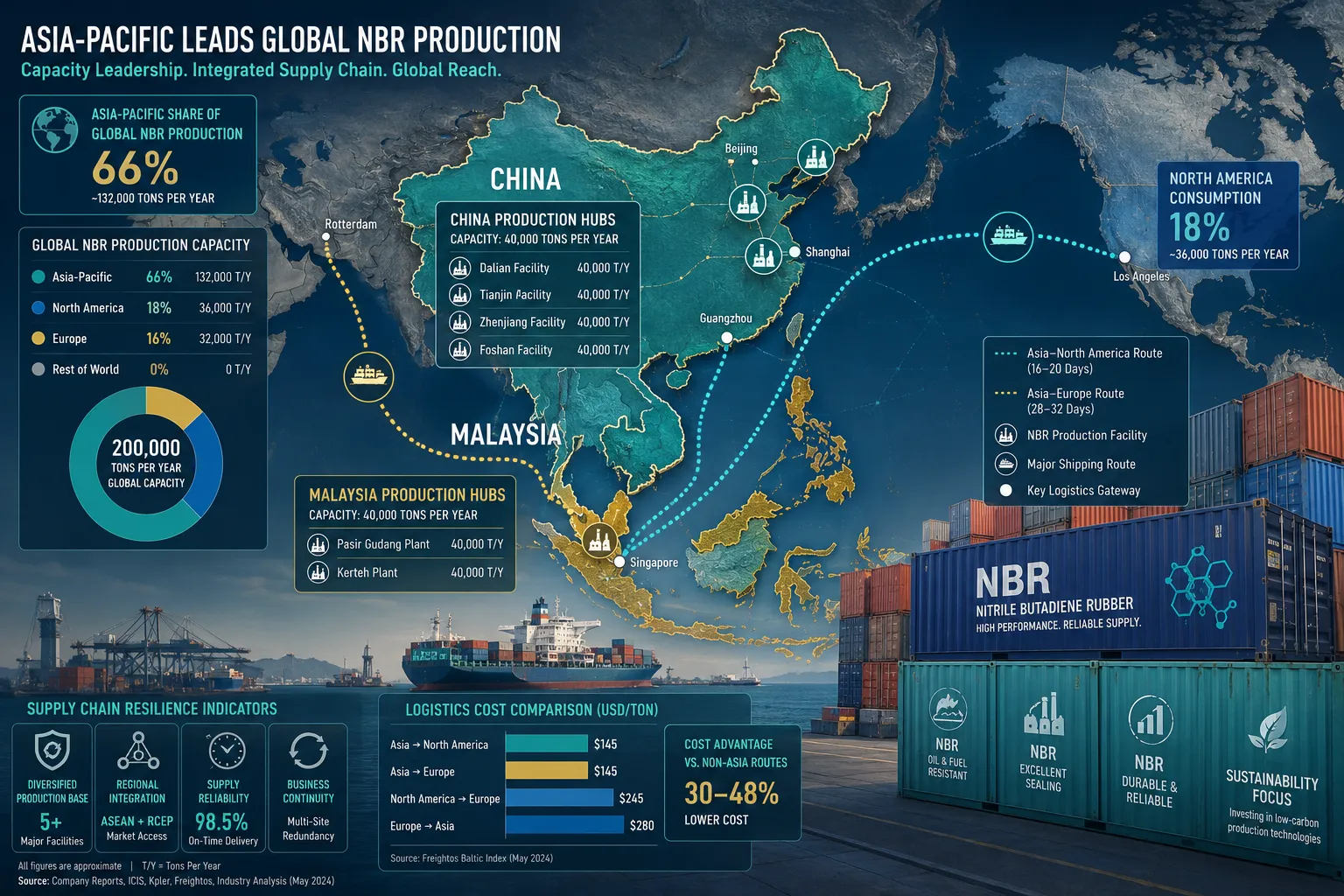

- Asia-Pacific holds nearly 58% of global NBR production capacity, driving regional integration strategies to reduce cross-border bottlenecks.

- Between 2023 and 2025, 27% of industry developments focused on capacity expansion, 22% on automation, and 31% on sustainability upgrades—all supporting cost efficiency.

- Analysts predict integrated players will outperform merchant-only producers during volatile cycles through 2033, as feedstock control becomes a defensive necessity.

Understanding Vertical NBR Integration in Nitrile Production

Vertical NBR Integration in Nitrile Production: How It Lowers Costs and Boosts Supply Stability refers to a business model where manufacturers own or control multiple stages of the nitrile butadiene rubber supply chain. Instead of purchasing raw materials on the open market, integrated producers secure direct access to butadiene and acrylonitrile feedstocks, operate their own polymerization facilities, and often extend downstream into compounding, latex production, and finished goods manufacturing such as nitrile gloves for hospitals.

This approach contrasts sharply with traditional merchant models, where each stage operates independently. In a merchant system, price volatility cascades through the chain: when butadiene spikes, monomer producers raise prices, which compounders pass to glove manufacturers, who ultimately face margin compression or must increase end-user prices. Integrated players bypass these cascading markups and gain predictability.

Key Components of Vertical Integration

Raw Material Procurement: Integrated producers often secure long-term contracts or own equity stakes in butadiene and acrylonitrile suppliers. Some even backward-integrate into petrochemical refining to guarantee feedstock availability.

Polymerization and Compounding: Owning NBR production facilities allows companies to optimize formulations for specific applications—whether oil-resistant gloves for automotive work or food-safe nitrile gloves for processing plants—without relying on third-party suppliers.

Downstream Manufacturing: Many integrated producers operate their own glove dipping lines or protective equipment factories, capturing margin at every stage and ensuring quality control from molecule to finished product.

Logistics and Distribution: Controlling transportation and warehousing reduces lead times and freight costs, particularly important when shipping between Asia-Pacific production hubs and North American or European markets.

How Vertical Integration Lowers Costs in Nitrile Production

The economic case for Vertical NBR Integration in Nitrile Production: How It Lowers Costs and Boosts Supply Stability rests on three pillars: feedstock cost control, operational efficiency, and margin capture.

Feedstock Cost Control

Raw materials represent 50% to 65% of total NBR production costs. When butadiene prices surged in early 2025, merchant buyers faced immediate margin pressure. Integrated producers with locked-in feedstock contracts or captive supply maintained stable input costs, preserving profitability even as spot markets fluctuated.

A concrete example: ARLANXEO and TSRC expanded their joint-venture NBR plant in Nantong, China, to approximately 40,000 tons per year in May 2025. By co-locating polymerization near feedstock sources and coordinating procurement, the partners reduced logistics costs and secured preferential pricing from regional butadiene suppliers.

Operational Efficiency and Automation

Between 2023 and 2025, 22% of reported industry developments involved automation investments. Integrated producers are pairing capacity expansion with process optimization—automated compounding lines, real-time quality monitoring, and predictive maintenance—to drive down per-unit costs.

Capacity utilization also improves when a single entity controls multiple stages. Instead of shipping intermediate products between facilities, integrated plants can move material seamlessly from polymerization to compounding to dipping, reducing handling, storage, and transportation expenses.

Margin Capture Across the Value Chain

Traditional supply chains fragment margin: feedstock suppliers, monomer producers, compounders, and glove manufacturers each take a cut. Vertical integration consolidates those margins under one roof. Industry analysts estimate that fully integrated producers can achieve 15% to 25% lower total cost of ownership compared to merchant-dependent competitors, a decisive advantage in commodity-sensitive markets.

Boosting Supply Stability Through Integration

Vertical NBR Integration in Nitrile Production: How It Lowers Costs and Boosts Supply Stability is equally about resilience as it is about cost. The COVID-19 pandemic exposed vulnerabilities in fragmented supply chains: border closures, port congestion, and raw-material shortages disrupted production globally. Integrated producers weathered these shocks more effectively.

Regional Supply Security

Asia-Pacific holds nearly 58% of global NBR production capacity, while North America accounts for 18% of consumption and Europe 16% of demand. This geographic mismatch creates dependency on cross-border logistics. Integrated producers are responding by establishing regional production clusters—combining feedstock sourcing, polymerization, and downstream manufacturing within a single market to reduce exposure to trade disruptions.

The ARLANXEO-TSRC Nantong expansion exemplifies this strategy: by producing NBR locally in China, the joint venture serves domestic glove manufacturers while also supporting global customers through a diversified footprint.

Quality Assurance and Compliance

Integrated producers control formulation and testing at every stage, ensuring consistency and compliance with regulatory standards. This is particularly valuable in medical and food-contact applications, where nitrile glove thickness and chemical resistance must meet strict specifications.

Recent product launches illustrate this trend: between 2023 and 2025, more than 40 new NBR latex formulations were introduced, many targeting oil resistance above 90% and elongation above 500%. Notably, 35% of these launches were accelerator-free, addressing allergic reactions affecting 8% to 12% of healthcare workers. Integrated producers can rapidly iterate on formulations and scale production without negotiating with external suppliers.

Long-Term Contract Stability

Buyers—whether glove manufacturers, automotive suppliers, or industrial distributors—increasingly prefer integrated suppliers who can guarantee multi-year availability and pricing predictability. Vertical integration enables producers to offer take-or-pay contracts and volume commitments that merchant suppliers cannot match, strengthening customer relationships and revenue visibility.

Leading Manufacturers’ Integration Strategies

ARLANXEO and TSRC Joint Venture

The May 2025 expansion of the Nantong plant represents a textbook case of vertical integration. ARLANXEO, a global synthetic rubber leader, partnered with TSRC, a major Taiwanese producer, to combine technical expertise, regional market access, and feedstock procurement leverage. The 40,000-ton facility supports both domestic Chinese demand and export markets, illustrating how integration can serve multiple geographies from a single hub.

Synthomer, Neste, and PCS Bio-Based Integration

In February 2025, Synthomer, Neste, and PCS created an ISCC-certified value chain for bio-based nitrile latexes. This initiative integrates renewable feedstock sourcing with latex production, targeting the glove industry’s growing demand for sustainable materials. By controlling the entire chain—from bio-based monomer supply through latex formulation—the consortium reduces dependency on fossil feedstocks and differentiates its products in a crowded market.

Capacity Expansion in Malaysia and China

Industry reports project that announced capacity additions in Malaysia and China through 2026–2028 could add roughly 320,000 metric tons of annual NBR latex capacity. Leading players are pairing these expansions with backward integration into monomer supply and forward integration into glove manufacturing, ensuring that new capacity translates into stable, profitable production rather than excess inventory.

Impact on Pricing Volatility Post-COVID

The pandemic triggered unprecedented volatility in nitrile markets. Glove demand surged, butadiene prices spiked, and logistics costs soared. Integrated producers demonstrated measurably better performance during this period.

Price Stability: Companies with captive feedstock supply maintained more stable pricing for customers, even as spot butadiene fluctuated by 40% or more quarter-over-quarter. This stability translated into stronger customer retention and market share gains.

Supply Continuity: Integrated producers avoided the production stoppages that plagued merchant-dependent competitors when feedstock shortages emerged. By controlling multiple stages, they could prioritize internal supply and maintain output.

Margin Resilience: While merchant producers saw margins compress during feedstock spikes, integrated players captured the spread between raw-material costs and finished-product prices, resulting in record profitability for some firms in 2021–2022.

As markets normalize in 2026, the lesson is clear: vertical integration provides a buffer against volatility, making it a strategic imperative rather than a tactical option.

Predictions for 2026–2033 Market Stability

Industry analysts expect Vertical NBR Integration in Nitrile Production: How It Lowers Costs and Boosts Supply Stability to accelerate through 2033, driven by several factors.

Continued Feedstock Volatility

Butadiene and acrylonitrile markets remain exposed to crude oil price swings, geopolitical tensions, and refinery capacity shifts. Analysts predict that feedstock volatility will persist, making integration an essential hedge for producers seeking predictable economics.

Regulatory and Sustainability Pressures

Governments and buyers are demanding greater transparency and sustainability in supply chains. Integrated producers can more easily track and certify feedstock origins, implement circular economy practices, and meet ESG (environmental, social, governance) criteria—advantages that will become increasingly valuable as regulations tighten.

Technological Advancements

Automation, digitalization, and process optimization will continue to drive cost reductions. Integrated producers are best positioned to invest in these technologies across multiple stages, compounding efficiency gains and widening the cost gap versus merchant competitors.

Market Consolidation

Analysts predict that smaller, non-integrated producers will struggle to compete on cost and supply reliability, leading to consolidation. Larger, vertically integrated players will acquire or partner with upstream and downstream firms, further concentrating the industry.

Growth in Specialized Applications

The latex segment is expected to grow at a 4.59% CAGR during 2026–2031, driven by medical glove demand and industrial applications. Integrated producers can rapidly develop and scale specialized formulations—such as accelerator-free latexes or oil-resistant grades—capturing premium pricing and margin.

Analyst Consensus: Firms that combine raw-material procurement, compounding, automation, and regional production are best positioned to absorb shocks from tariffs, freight disruption, and feedstock swings. Vertical integration is evolving from a growth strategy into a defensive necessity, ensuring that integrated players outperform merchant-only producers during volatile cycles.

Challenges and Considerations

While Vertical NBR Integration in Nitrile Production: How It Lowers Costs and Boosts Supply Stability offers clear advantages, it also presents challenges.

Capital Intensity: Building or acquiring facilities across multiple stages requires significant upfront investment. Smaller producers may lack the financial resources to integrate, limiting this strategy to larger players.

Operational Complexity: Managing polymerization, compounding, and downstream manufacturing demands diverse technical expertise and coordination. Integration can strain management bandwidth and increase operational risk if not executed well.

Market Flexibility: Integrated producers may face reduced flexibility to switch suppliers or adjust sourcing strategies in response to market changes. Long-term feedstock contracts can become liabilities if spot prices fall significantly.

Regulatory and Antitrust Scrutiny: In some markets, vertical integration may attract regulatory attention, particularly if it leads to market concentration or anti-competitive behavior.

Despite these challenges, the strategic benefits—cost control, supply security, and margin capture—make vertical integration an increasingly attractive model for leading NBR producers.

Conclusion

Vertical NBR Integration in Nitrile Production: How It Lowers Costs and Boosts Supply Stability has transitioned from a competitive advantage to a strategic imperative in 2026. As raw-material volatility persists, logistics remain fragile, and buyers demand greater supply certainty, integrated producers are demonstrably outperforming merchant-dependent competitors. By controlling feedstock procurement, polymerization, compounding, and downstream manufacturing, companies reduce costs by 15% to 25%, ensure supply continuity, and capture margin at every stage.

Leading manufacturers—from ARLANXEO and TSRC’s Nantong expansion to Synthomer’s bio-based integration—are proving that vertical integration delivers measurable economic and operational benefits. Looking ahead to 2033, analysts predict that integrated players will continue to gain market share, drive consolidation, and set the standard for cost efficiency and supply resilience.

For manufacturers: Evaluate opportunities to integrate backward into feedstock supply or forward into finished goods. Prioritize automation and process optimization to maximize efficiency gains across the value chain.

For buyers: Partner with integrated suppliers who can offer long-term pricing stability, guaranteed availability, and consistent quality. Assess suppliers’ vertical integration capabilities as a key criterion in procurement decisions.

For investors: Focus on companies with demonstrated integration strategies, regional production footprints, and strong balance sheets to fund continued expansion. Vertical integration is the defining competitive moat in nitrile production for the decade ahead.

SEO Meta Title: Vertical NBR Integration Cuts Costs & Boosts Supply Stability