Last updated: June 25, 2026

Quick Answer

Synthetic rubber price hedging for nitrile glove buyers involves using financial instruments like futures contracts, fixed-price supplier agreements, and strategic inventory management to lock in raw material costs and protect against the 30-50% price swings common in butadiene and acrylonitrile markets. Buyers can stabilize their cost structure by hedging 40-70% of their expected raw material needs for 6-12 months ahead, balancing protection against downside flexibility. This approach is particularly valuable for mid-to-large volume buyers who need predictable pricing for contract bidding and budget planning.

Key Takeaways

- Nitrile glove production costs are heavily influenced by synthetic rubber prices, which can swing 30-50% annually due to crude oil volatility and supply chain disruptions

- Hedging strategies include futures contracts, fixed-price supplier agreements, options contracts, and strategic inventory positioning

- Most successful buyers hedge 40-70% of their raw material needs rather than 100%, maintaining flexibility for spot market opportunities

- Small buyers under 500,000 gloves monthly may find supplier agreements more practical than direct commodity hedging due to minimum contract sizes

- Timing matters: hedge when prices are historically low or stable, not during panic buying periods

- Common mistakes include over-hedging, ignoring basis risk, and failing to match hedge duration with actual consumption patterns

- Hedging costs typically range from 2-5% of the contract value but can prevent 20-40% cost increases during supply shocks

- Buyers need clear consumption forecasts, working capital for margin requirements, and internal processes to manage hedge positions

What Is Synthetic Rubber Price Hedging for Nitrile Glove Manufacturers

Synthetic rubber price hedging for nitrile glove manufacturers is a risk management strategy that uses financial instruments or contractual agreements to lock in future prices for the key raw materials—butadiene and acrylonitrile—that make up nitrile rubber. This protects buyers from unexpected price increases that can erode profit margins or make contract pricing unprofitable.

Nitrile gloves are made from synthetic rubber created by polymerizing butadiene and acrylonitrile, both petroleum-derived chemicals. When crude oil prices spike or refinery capacity tightens, these raw material costs can jump 40% or more within weeks. For a glove buyer who committed to a six-month supply contract at fixed prices, such increases can turn profitable deals into losses.

Hedging creates a financial offset. If raw material prices rise, the hedge position gains value and compensates for higher physical costs. If prices fall, the hedge loses value but the buyer benefits from cheaper spot market purchases. The goal is not to profit from speculation but to achieve cost predictability.

Key components of a hedging program:

- Identifying price exposure based on monthly consumption volumes

- Selecting appropriate hedging instruments (futures, options, swaps, or supplier contracts)

- Determining hedge ratio (what percentage of needs to hedge)

- Setting hedge duration aligned with production schedules

- Monitoring positions and adjusting as market conditions change

Choose hedging if your business requires stable pricing for contract bidding, has sufficient volume to justify transaction costs, and can manage the administrative complexity. Skip it if you operate on spot market pricing with pass-through clauses or have very small volumes where hedging costs exceed benefits.

How Does Commodity Hedging Work for Nitrile Glove Buyers

Commodity hedging works by taking an offsetting position in a financial market that moves inversely to your physical raw material costs. When you buy nitrile gloves or their raw materials, you simultaneously take a futures or options position that gains value if prices rise, offsetting your increased physical costs.

The mechanics depend on the instrument used. With futures contracts, you agree to buy a specific quantity of butadiene or acrylonitrile at a set price on a future date. If spot prices rise above your futures price, you can sell the contract at a profit or take physical delivery at the lower locked-in price. If prices fall, you lose on the futures position but pay less for physical materials.

Step-by-step hedging process:

- Calculate exposure: Determine monthly raw material needs in metric tons based on glove production forecasts

- Select instruments: Choose between exchange-traded futures, OTC swaps, supplier fixed-price contracts, or options

- Determine hedge ratio: Decide what percentage to hedge (typically 40-70% for balanced protection)

- Execute positions: Open contracts through a commodity broker or negotiate supplier agreements

- Monitor and adjust: Track basis (difference between futures and physical prices), margin requirements, and consumption patterns

- Close positions: Offset futures contracts before expiry or take physical delivery if structured that way

Common mistake: Hedging 100% of expected needs leaves no flexibility if consumption drops or spot prices fall significantly. Most experienced buyers hedge 50-60% of core needs and buy the remainder on the spot market.

The effectiveness depends on correlation between the hedging instrument and your actual costs. If you hedge crude oil futures but your supplier’s pricing formula uses a different benchmark, basis risk can reduce hedge effectiveness.

What Are the Main Costs in Nitrile Glove Production

The main costs in nitrile glove production are raw materials (60-70% of total cost), manufacturing and labor (15-20%), energy (5-8%), and logistics (5-10%). Raw materials dominate the cost structure, with butadiene and acrylonitrile accounting for roughly 35% and 28% of total production costs respectively.

Detailed cost breakdown for nitrile glove production:

| Cost Component | Percentage of Total | Volatility Level | Hedgeable |

|---|---|---|---|

| Butadiene | 35% | High (30-50% annual swings) | Yes |

| Acrylonitrile | 28% | High (25-45% annual swings) | Yes |

| Processing chemicals | 7% | Low to moderate | Limited |

| Manufacturing labor | 12% | Low | No |

| Energy (natural gas, electricity) | 6% | Moderate to high | Yes |

| Packaging materials | 4% | Low | No |

| Logistics and freight | 8% | Moderate | Partially |

Butadiene and acrylonitrile prices track crude oil and natural gas prices with a lag, but also respond to refinery capacity, demand from tire and automotive industries, and regional supply disruptions. During the 2020-2021 period, butadiene prices in Asia doubled from $800 to $1,600 per metric ton due to refinery shutdowns and demand surges.

For a buyer purchasing 1 million gloves monthly, a 20% increase in synthetic rubber prices translates to roughly $15,000-20,000 in additional monthly costs. Over a year, that’s $180,000-240,000 in margin erosion if selling prices can’t be adjusted.

Choose to hedge raw materials if:

- Raw materials represent more than 50% of your cost structure

- You operate on fixed-price contracts with customers

- Your business can’t quickly pass through cost increases

- You need predictable costs for financial planning and credit arrangements

Energy costs can also be hedged through natural gas futures if your supplier passes through energy surcharges, but this is less common for glove buyers than direct raw material hedging.

Nitrile Glove Price Hedging vs Spot Market Buying: Which Is Better

Neither hedging nor spot market buying is universally better—the right choice depends on your business model, risk tolerance, volume, and market outlook. Hedging provides cost certainty and budget predictability but caps your upside if prices fall, while spot buying offers flexibility and potential savings but exposes you to sudden price spikes.

Hedging is better when:

- You bid on long-term supply contracts with fixed pricing

- Your business operates on thin margins where a 15-20% cost increase causes losses

- You need stable costs for financial planning, loan covenants, or investor commitments

- You purchase large volumes (500,000+ gloves monthly) where hedging costs are proportionally small

- Market conditions show high volatility or upward price trends

Spot market buying is better when:

- You have pass-through pricing clauses with customers

- Your volumes are small (under 200,000 gloves monthly) making hedging transaction costs prohibitive

- You maintain flexible inventory and can time purchases strategically

- Current prices are historically high and you expect mean reversion

- Your business model prioritizes agility over predictability

Hybrid approach (recommended for most mid-size buyers): Hedge 40-60% of expected needs for the next 6-12 months to establish a cost floor, then buy the remainder on the spot market. This balances protection with flexibility. If prices rise, your hedged portion limits damage. If prices fall, your unhedged portion captures savings.

A medical supply distributor buying 800,000 nitrile gloves monthly might hedge 500,000 gloves’ worth of raw materials through six-month futures contracts, then purchase the remaining 300,000 gloves’ worth monthly based on current prices. This approach prevented 30% cost increases during the 2021 supply crisis while still allowing 15% savings when prices normalized in late 2022.

Common mistake: Switching strategies based on recent price movements. Buyers who hedge only after prices have already spiked miss the protection window, while those who abandon hedging after one quarter of falling prices expose themselves to the next spike.

How to Lock in Synthetic Rubber Prices for Glove Manufacturing

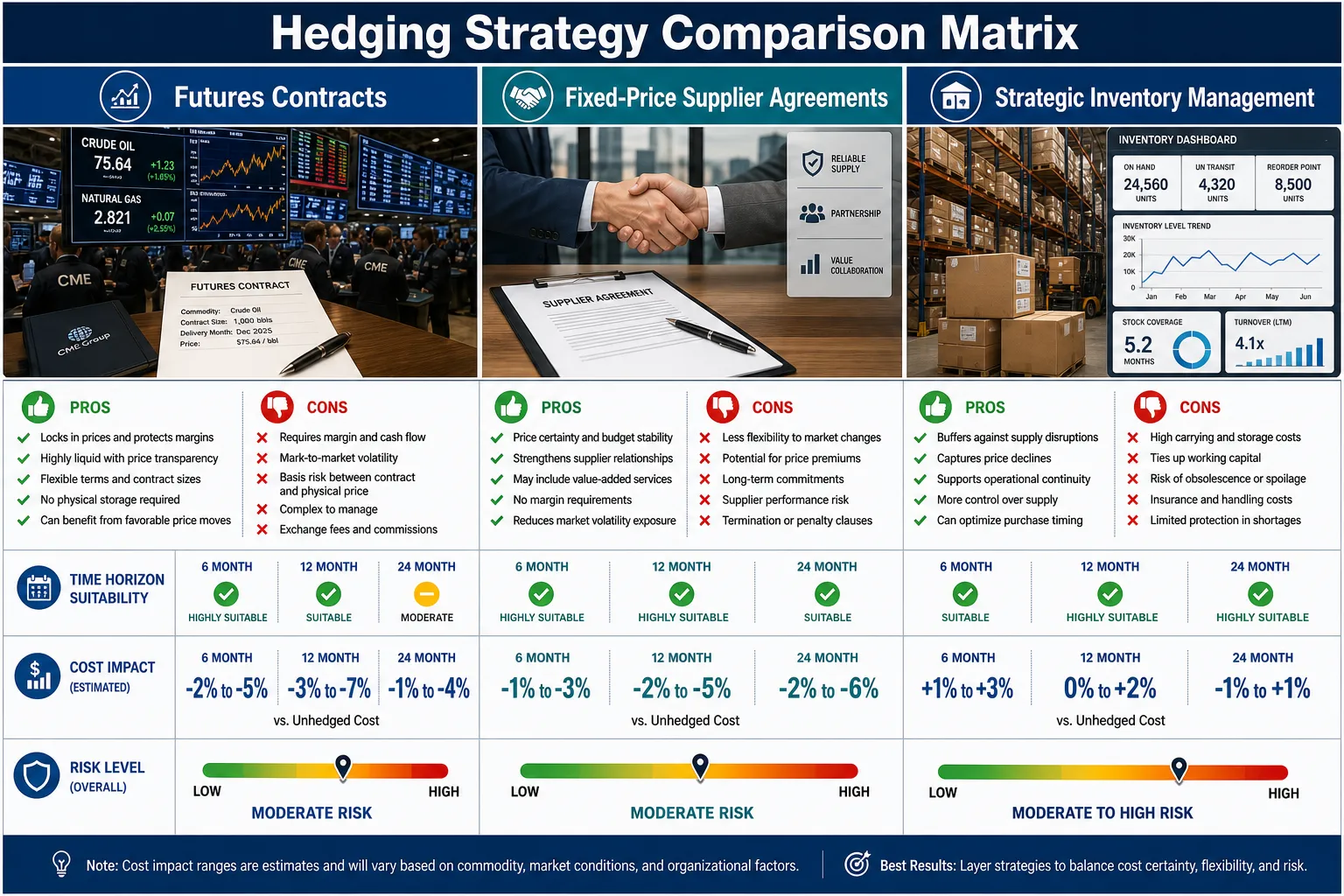

To lock in synthetic rubber prices for glove manufacturing, use fixed-price supplier contracts, commodity futures contracts, or options strategies that guarantee maximum prices for 6-12 months ahead. The most practical approach for most buyers is negotiating fixed-price agreements with glove suppliers or raw material distributors who handle the commodity hedging themselves.

Method 1: Fixed-price supplier agreements

Negotiate contracts with your glove supplier that lock in prices for a specific volume and timeframe. The supplier manages the commodity risk and builds hedging costs into the price. This works best for buyers who lack commodity trading expertise or minimum volumes for direct futures trading.

- Typical duration: 3-12 months

- Minimum volumes: Usually 100,000-500,000 gloves monthly

- Premium cost: 3-7% above spot prices

- Best for: Small to mid-size buyers without commodity trading infrastructure

Method 2: Direct commodity futures contracts

Open positions in butadiene or crude oil futures through a commodity broker. This requires understanding contract specifications, margin requirements, and daily mark-to-market settlements.

- Typical contract size: 25-50 metric tons per contract

- Margin requirements: 5-15% of contract value

- Trading costs: $50-200 per contract plus broker fees

- Best for: Large buyers with 1+ million gloves monthly consumption and financial expertise

Method 3: Options contracts

Buy call options that give you the right (but not obligation) to purchase raw materials at a set price. This provides upside protection while preserving downside flexibility if prices fall.

- Premium cost: 2-8% of contract value depending on strike price and duration

- No margin calls if prices move against you

- Best for: Buyers who want protection against spikes but don’t want to lock in current prices

Method 4: Strategic inventory positioning

When prices are historically low, increase inventory levels to 90-120 days rather than the typical 30-45 days. This “physical hedge” locks in low prices through inventory investment.

- Capital requirement: Significant working capital needed

- Storage costs: 1-3% monthly for proper warehouse conditions

- Risk: Product obsolescence, quality degradation, or further price declines

- Best for: Buyers with strong cash positions during confirmed price troughs

Implementation steps:

- Calculate your monthly raw material equivalent based on glove consumption (roughly 4-5 kg synthetic rubber per 1,000 gloves)

- Determine hedge horizon based on your contract commitments (6 months for most buyers)

- Request fixed-price quotes from 3-5 suppliers for comparison

- If going direct to futures, open a commodity trading account with a reputable broker

- Execute positions in stages (layer in over 4-6 weeks) rather than all at once to average entry prices

- Document hedge rationale and monitor monthly against physical consumption

Choose fixed-price supplier agreements if you’re new to hedging or have volumes under 500,000 gloves monthly. Move to direct futures only when you have dedicated procurement staff and sufficient volume to justify the complexity.

What Hedging Instruments Are Available for Butadiene and Acrylonitrile Prices

The primary hedging instruments for butadiene and acrylonitrile prices are crude oil futures (as a proxy), naphtha futures, direct butadiene swaps in OTC markets, and supplier fixed-price contracts. Direct exchange-traded futures for butadiene and acrylonitrile are limited, so most hedgers use correlated commodities or bilateral agreements.

Available instruments ranked by accessibility:

1. Crude oil futures (WTI or Brent)

- Exchange: NYMEX, ICE

- Correlation to butadiene: 0.65-0.75 (moderate to strong)

- Contract size: 1,000 barrels

- Liquidity: Excellent

- Best for: Large buyers hedging broad petrochemical exposure

- Limitation: Basis risk—crude oil doesn’t perfectly track butadiene due to refinery capacity and regional factors

2. Naphtha futures

- Exchange: TOCOM (Tokyo), Platts assessments

- Correlation to butadiene: 0.70-0.80 (strong)

- Contract size: 50 kiloliters (TOCOM)

- Liquidity: Moderate

- Best for: Asian market buyers with direct naphtha-to-chemicals exposure

- Limitation: Less liquid than crude oil, requires specialized broker access

3. OTC butadiene swaps

- Market: Over-the-counter through commodity brokers

- Correlation: 1.0 (direct)

- Contract size: Customizable (typically 100+ metric tons)

- Liquidity: Limited to moderate

- Best for: Large industrial buyers with established banking relationships

- Limitation: Requires credit lines, counterparty risk, less transparent pricing

4. Fixed-price supplier contracts

- Market: Direct negotiation with chemical distributors or glove manufacturers

- Correlation: 1.0 (direct)

- Contract size: Flexible based on consumption

- Liquidity: N/A

- Best for: All buyer sizes, especially those under 1 million gloves monthly

- Limitation: Limited negotiating leverage for small buyers, supplier credit risk

5. Options on crude oil or naphtha

- Exchange: NYMEX, ICE

- Provides asymmetric protection (caps upside cost, preserves downside savings)

- Premium cost: 3-8% of notional value

- Best for: Buyers wanting protection without full commitment

- Limitation: Premium cost reduces savings if prices remain stable

Practical recommendation by buyer size:

- Under 200,000 gloves monthly: Fixed-price supplier contracts only

- 200,000-1,000,000 gloves monthly: Fixed-price contracts plus crude oil futures for partial hedge

- Over 1,000,000 gloves monthly: Combination of crude oil futures, naphtha futures, and OTC swaps for precision

Common mistake: Hedging with crude oil futures without understanding basis risk. During regional supply disruptions, butadiene prices can spike 30% while crude oil remains stable, leaving your hedge ineffective. Always test historical correlation for your specific supplier’s pricing formula before committing to a proxy hedge.

Common Mistakes When Hedging Raw Material Costs for Nitrile Gloves

The most common mistakes when hedging raw material costs for nitrile gloves are over-hedging beyond actual consumption, ignoring basis risk between hedge instruments and physical prices, poor timing of hedge entry, and failing to match hedge duration with contract commitments. These errors can turn risk management into speculative losses.

Critical mistakes to avoid:

1. Over-hedging (hedging more than you’ll actually consume) If you hedge for 1 million gloves monthly but only sell 700,000, you’re left with 300,000 gloves’ worth of speculative positions. When prices fall, you lose on the hedge without offsetting physical savings. Hedge 60-70% of minimum expected consumption, not optimistic forecasts.

2. Ignoring basis risk Hedging crude oil when your supplier prices off regional butadiene assessments creates basis risk. During the 2020 supply crisis, Asian butadiene prices spiked 45% while WTI crude rose only 20%, leaving hedgers with 25% unprotected exposure. Always verify correlation between your hedge instrument and actual supplier pricing formula.

3. Panic hedging at price peaks Buyers who wait until prices have already spiked 30-40% lock in high costs and miss the protection window. Hedge when prices are stable or declining, not during panic buying. Set predetermined price triggers (e.g., “hedge when butadiene falls below $1,200/MT”) rather than reacting emotionally.

4. Mismatched hedge duration Opening 12-month futures positions when your customer contracts are only 6 months creates exposure in months 7-12. If demand drops or contracts aren’t renewed, you’re stuck with speculative positions. Match hedge expiration to your actual commitment timeline.

5. Insufficient working capital for margin calls Futures contracts require daily margin settlements. If prices move against your position, you must post additional cash. A buyer who hedged with 90% of available working capital faced margin calls that forced early liquidation at a loss. Reserve 20-30% of hedge value as margin buffer.

6. Neglecting to document hedge rationale Without clear documentation of why you hedged, at what price, and for what volume, it’s impossible to evaluate effectiveness or learn from mistakes. Maintain a hedge log with entry rationale, target exit conditions, and monthly performance reviews.

7. Treating hedging as profit center Hedging is risk management, not speculation. Buyers who try to “time the market” or over-trade based on price predictions usually underperform simple, disciplined hedge-and-hold strategies. Set hedge policy based on business needs, not market views.

8. Ignoring storage and quality constraints Physical hedging through inventory buildup fails if you lack proper storage for nitrile gloves or if products degrade before use. Nitrile gloves have 3-5 year shelf life under proper conditions, but humidity and heat can reduce quality. Calculate storage costs and quality risk before committing to inventory hedges.

Real example: A mid-size medical distributor hedged 100% of expected annual butadiene needs in Q1 2022 when prices were elevated. When demand dropped 30% due to post-pandemic normalization and prices fell 35%, they faced $180,000 in hedge losses with no offsetting physical savings. A 50% hedge ratio would have limited losses to $90,000 while still capturing $105,000 in spot market savings.

Is Price Hedging Worth It for Small Nitrile Glove Buyers

Price hedging is typically not worth it for small nitrile glove buyers purchasing under 200,000 gloves monthly due to high transaction costs, minimum contract sizes, and administrative complexity that outweigh the benefits. However, small buyers can achieve similar protection through fixed-price supplier agreements that bundle hedging into the purchase price.

Cost-benefit analysis for small buyers:

Direct commodity hedging costs include:

- Broker fees: $500-2,000 monthly minimum

- Trading commissions: $50-200 per contract

- Margin requirements: 5-15% of contract value tied up in cash

- Staff time: 10-20 hours monthly for monitoring and administration

- Software and data: $200-500 monthly for market data and analysis tools

For a buyer purchasing 150,000 gloves monthly (roughly $15,000-20,000 in raw material exposure), these costs represent 3-5% of the hedged value—too high to justify for typical 10-20% price swings.

Better alternatives for small buyers:

1. Fixed-price supplier contracts Your glove supplier or distributor handles commodity hedging and builds the cost into pricing. You pay a 2-4% premium over spot prices but avoid all administrative complexity. This is the most practical solution for buyers under 500,000 gloves monthly.

2. Quarterly price reviews with caps Negotiate contracts with quarterly price adjustments based on published indices, but with maximum increase caps (e.g., “prices adjust quarterly based on Platts butadiene assessment, capped at 15% per quarter”). This limits extreme spikes while allowing some price flexibility.

3. Volume commitments for price stability Commit to minimum purchase volumes in exchange for price stability. Suppliers often offer 6-12 month fixed pricing for buyers who guarantee minimum monthly purchases, effectively sharing hedging benefits.

4. Buying cooperatives Join with other small buyers to achieve volumes that justify direct hedging or improve negotiating leverage with suppliers. Several regional medical supply cooperatives aggregate member demand to negotiate better terms.

When small buyers should consider hedging:

- You have very thin margins (under 10%) where a 15% cost increase causes losses

- You’ve secured long-term fixed-price contracts with customers

- You have financial expertise in-house or can partner with a commodity advisor

- Your supplier refuses fixed-price agreements or charges excessive premiums (over 8%)

Choose fixed-price supplier agreements if: You’re under 500,000 gloves monthly, lack commodity trading experience, or want to focus on core business rather than financial risk management.

Consider direct hedging only if: You exceed 1 million gloves monthly, have dedicated procurement staff, and can negotiate better terms than your supplier’s bundled pricing.

What Happens If Synthetic Rubber Prices Drop After I Hedge

If synthetic rubber prices drop after you hedge, you’ll lose money on your hedge position but pay less for physical raw materials, resulting in a net position close to your original hedged price. The hedge loss is an opportunity cost—you gave up potential savings in exchange for price certainty and protection against increases.

Scenario example:

You hedge 60% of your annual butadiene needs at $1,400 per metric ton through futures contracts. Six months later, spot prices fall to $1,100 per metric ton.

- Hedged portion (60%): You pay $1,400/MT through your futures position (or your supplier charges $1,400/MT under fixed-price contract)

- Unhedged portion (40%): You buy at spot price of $1,100/MT

- Blended cost: (0.60 × $1,400) + (0.40 × $1,100) = $840 + $440 = $1,280/MT

- Opportunity cost: $1,280 – $1,100 = $180/MT on your total volume

Your competitor who didn’t hedge pays $1,100/MT and has a $180/MT cost advantage. However, if prices had risen to $1,700/MT instead, you’d have a $420/MT advantage on your hedged portion.

How to manage downside scenarios:

1. Partial hedging (40-70% of needs) Never hedge 100% of expected consumption. This preserves flexibility to capture some savings if prices fall while still protecting against increases. Most sophisticated buyers hedge 50-60% of core needs.

2. Options instead of futures Buy call options that cap your maximum price but allow you to benefit if prices fall (minus the premium paid). This costs 3-8% upfront but provides asymmetric protection.

3. Layered entry Instead of hedging all at once, layer in positions over 2-3 months. This averages your entry price and reduces regret if you hedge right before a price drop.

4. Dynamic hedging Adjust hedge ratios based on price levels. Hedge more (60-70%) when prices are low to moderate, less (30-40%) when prices are historically high. This requires discipline to avoid emotional decision-making.

5. Accept opportunity cost as insurance premium Reframe hedge losses as insurance premiums. You paid for price certainty and protection against catastrophic increases. Just as you don’t regret home insurance premiums when your house doesn’t burn down, don’t regret hedge costs when prices fall.

Common psychological trap: Buyers who experience hedge losses when prices fall often abandon hedging entirely, leaving themselves exposed when prices spike again. Maintain consistent hedge discipline based on business needs, not recent price movements.

Real example: A hospital supply buyer hedged 50% of annual nitrile glove needs in early 2022 at elevated prices. When prices fell 30% by late 2022, they faced $85,000 in hedge losses but saved $120,000 on unhedged purchases, netting $35,000 savings versus full hedging. More importantly, the hedge prevented catastrophic losses during the 2020-2021 spike that bankrupted several competitors.

How Long Should Nitrile Glove Manufacturers Hedge Their Rubber Costs

Nitrile glove manufacturers should hedge their rubber costs for 6-12 months ahead, matching the duration to their customer contract commitments and production planning horizon. Shorter hedges (3-6 months) work for spot market buyers with flexible pricing, while longer hedges (12-18 months) suit manufacturers with long-term fixed-price supply agreements.

Optimal hedge duration by business model:

Spot market buyers with pass-through pricing: 0-3 months If you can adjust prices monthly based on current costs, minimal hedging is needed. Consider short-term hedges only during periods of extreme volatility to smooth month-to-month fluctuations.

Distributors with quarterly contracts: 6-9 months Hedge at least two quarters ahead to cover current commitments plus one buffer quarter. This protects existing contracts while allowing flexibility for future pricing adjustments.

Manufacturers with annual supply agreements: 12-15 months Hedge the full contract duration plus 3 months buffer for production planning. If you’ve committed to supply 1 million gloves monthly at fixed prices for 12 months, hedge 12-15 months of raw materials.

Large institutional buyers with multi-year contracts: 12-24 months rolling Implement a rolling hedge program where you’re always hedged 12-24 months forward, adding new positions quarterly as old ones expire. This provides continuous protection without excessive long-term exposure.

Factors that influence optimal duration:

- Customer contract length (match hedge to commitments)

- Price volatility (higher volatility favors longer hedges for stability)

- Working capital availability (longer hedges tie up more margin)

- Market conditions (hedge longer when prices are favorable, shorter when elevated)

- Inventory turnover (faster turnover allows shorter hedges)

Common mistake: Hedging beyond your actual visibility. If you hedge 24 months forward but only have 12 months of confirmed orders, you’re speculating on months 13-24. Hedge only what you can reasonably forecast with 70%+ confidence.

Rolling hedge strategy (recommended for most buyers):

Maintain a continuous hedge program where you’re always covered 6-12 months forward:

- Month 1: Hedge months 7-12 at 60% of expected needs

- Month 4: Hedge months 13-18 at 40% of expected needs

- Month 7: Hedge months 19-24 at 40% of expected needs

- Adjust percentages based on price levels and order visibility

This approach provides consistent protection without requiring perfect long-term forecasts.

When to extend hedge duration:

- Prices are at multi-year lows (lock in favorable costs longer)

- You’ve secured long-term customer contracts at good margins

- Market indicators suggest supply tightening ahead

- You have strong working capital to support longer positions

When to shorten hedge duration:

- Prices are at multi-year highs (avoid locking in peak costs)

- Demand visibility is poor or declining

- Working capital is constrained

- You expect mean reversion to lower prices

For most mid-size nitrile glove buyers, a 6-9 month hedge horizon covering 50-60% of expected needs provides the best balance of protection, flexibility, and capital efficiency.

Alternatives to Futures Contracts for Managing Nitrile Glove Material Costs

The main alternatives to futures contracts for managing nitrile glove material costs are fixed-price supplier agreements, options contracts, commodity swaps, strategic inventory management, and vertical integration. Each offers different trade-offs between cost, complexity, flexibility, and protection level.

Alternative 1: Fixed-price supplier agreements

Negotiate contracts where your glove supplier or raw material distributor guarantees prices for 6-12 months. The supplier manages commodity risk and builds hedging costs into pricing.

- Complexity: Low (simple contract negotiation)

- Cost: 2-5% premium over spot prices

- Protection: Complete price certainty for contract duration

- Flexibility: Low (committed to volume and price)

- Best for: Small to mid-size buyers, those without commodity expertise

- Limitation: Supplier credit risk, limited negotiating leverage for small volumes

Alternative 2: Options contracts (calls and collars)

Buy call options that cap your maximum price while preserving ability to benefit from price decreases. Collars combine buying calls with selling puts to reduce premium cost.

- Complexity: Moderate (requires options understanding)

- Cost: 3-8% premium for calls, 1-3% for collars

- Protection: Asymmetric (caps upside, preserves downside)

- Flexibility: High (can let options expire if prices fall)

- Best for: Buyers wanting protection without full commitment

- Limitation: Premium cost reduces savings in stable markets

Alternative 3: Commodity swaps

Over-the-counter agreements to exchange floating prices for fixed prices with a counterparty (usually a bank or commodity trader).

- Complexity: High (requires credit lines, legal agreements)

- Cost: Bid-ask spread plus counterparty credit charges

- Protection: Complete price certainty

- Flexibility: Low (difficult to exit early)

- Best for: Large buyers with banking relationships

- Limitation: Counterparty risk, less transparent than exchange-traded futures

Alternative 4: Strategic inventory management

Increase inventory levels to 90-120 days when prices are historically low, effectively “buying forward” physically rather than financially.

- Complexity: Low (operational decision)

- Cost: Working capital tied up plus storage costs (1-3% monthly)

- Protection: Locks in low prices through physical ownership

- Flexibility: Moderate (can adjust consumption rate)

- Best for: Buyers with strong cash positions and storage capacity

- Limitation: Capital intensive, quality degradation risk, further price declines possible

Alternative 5: Vertical integration

Invest in or partner with synthetic rubber producers to secure supply at cost-plus pricing rather than market rates.

- Complexity: Very high (requires major capital investment)

- Cost: Significant upfront investment, ongoing operational involvement

- Protection: Complete control over supply and pricing

- Flexibility: Low (long-term commitment)

- Best for: Very large manufacturers with multi-billion dollar scale

- Limitation: Requires expertise outside core business, capital intensive

Alternative 6: Index-linked pricing with caps

Negotiate contracts where prices adjust based on published commodity indices but with maximum increase caps (e.g., “price = 1.2 × Platts butadiene assessment, capped at 15% quarterly increase”).

- Complexity: Low to moderate (contract negotiation)

- Cost: Minimal (built into pricing formula)

- Protection: Partial (caps extreme spikes, allows moderate increases)

- Flexibility: High (prices can decrease)

- Best for: Buyers wanting some protection without full hedging commitment

- Limitation: Doesn’t prevent gradual price increases within cap limits

Alternative 7: Diversified supplier base

Maintain relationships with 3-5 suppliers across different regions to create competition and reduce dependence on any single source.

- Complexity: Moderate (relationship management)

- Cost: Minimal (may sacrifice volume discounts)

- Protection: Reduces supply disruption risk, improves negotiating leverage

- Flexibility: High (can shift volumes based on pricing)

- Best for: All buyer sizes

- Limitation: Doesn’t directly hedge price risk, requires minimum volumes per supplier

Recommended approach by buyer profile:

- Small buyers (under 200,000 gloves monthly): Fixed-price supplier agreements + diversified supplier base

- Mid-size buyers (200,000-1,000,000 monthly): Fixed-price agreements for 50% + strategic inventory for 20% + spot market for 30%

- Large buyers (over 1,000,000 monthly): Futures or swaps for 40% + options for 20% + fixed-price agreements for 20% + spot market for 20%

Most successful buyers combine multiple approaches rather than relying on a single strategy, creating a layered risk management program that balances cost, protection, and flexibility.

When Is the Best Time to Hedge Synthetic Rubber Prices

The best time to hedge synthetic rubber prices is when prices are at or below historical averages, volatility is moderate, and you have clear visibility into future consumption needs for the next 6-12 months. Avoid hedging during panic buying periods when prices have already spiked 30-40% above normal levels, as you’ll lock in peak costs.

Optimal hedging conditions:

1. Price level indicators

- Butadiene prices below $1,300/MT (Asian markets) or in bottom 40% of 5-year range

- Crude oil prices stable or declining (WTI below $75/barrel)

- Spread between crude oil and butadiene at normal historical ratios (2.5-3.5x)

2. Market structure signals

- Futures curve in contango (future prices higher than spot), indicating stable supply

- Low volatility (price swings under 10% monthly)

- Refinery utilization rates above 85% (indicates stable production)

3. Business timing factors

- 3-6 months before major contract renewals or bidding cycles

- When you have confirmed orders covering 70%+ of the hedge period

- After completing annual budgeting when consumption forecasts are clear

- When working capital is strong enough to support margin requirements

4. Seasonal patterns

- Q4 (October-December) often sees lower prices as demand softens before year-end

- Q2 (April-June) can offer opportunities before summer driving season increases crude oil demand

- Avoid hedging during Q1 (January-March) when post-holiday restocking drives prices up

Warning signs to delay hedging:

- Prices have spiked 30%+ in the past 3 months (likely at temporary peak)

- Major supply disruptions or geopolitical events creating panic buying

- Your own demand forecast uncertainty exceeds 30%

- Working capital constraints limit ability to meet margin calls

- Futures curve in steep backwardation (spot prices higher than future), suggesting supply crisis

Practical implementation:

Rather than trying to time the perfect entry, use a layered approach:

Month 1: Hedge 20% of 6-12 month needs at current prices Month 2: Add another 20% if prices remain stable or decline Month 3: Add final 20% to reach 60% total hedge ratio Ongoing: Maintain 50-60% rolling hedge, adding positions quarterly

This dollar-cost averaging approach reduces timing risk and prevents regret from hedging all at once before a price drop.

Real example: A medical distributor tracked butadiene prices monthly and set a trigger to hedge when prices fell below $1,250/MT. In Q4 2022, prices hit $1,180/MT and they hedged 50% of 2023 needs. Prices rose to $1,450/MT by Q2 2023, saving them $135,000 versus unhedged competitors. The key was having a predetermined trigger rather than trying to guess the absolute bottom.

Common mistake: Waiting for the “perfect” price that never comes. If prices are in the bottom 40% of historical range and you have clear consumption needs, hedge a portion (30-40%) even if you think prices might go lower. You can always add more later if prices decline further.

Do I Need a Broker to Hedge Nitrile Glove Raw Material Costs

You need a commodity broker to hedge nitrile glove raw material costs if you’re trading exchange-listed futures or options contracts, but not if you’re using fixed-price supplier agreements or strategic inventory management. For most small to mid-size buyers, working through suppliers who handle hedging internally is more practical than direct commodity trading.

When you need a broker:

Trading futures or options on exchanges (NYMEX, ICE, TOCOM)

- Brokers provide access to exchanges and handle trade execution

- They manage margin accounts and daily settlements

- They offer market research, price alerts, and hedging advice

- Cost: $500-2,000 monthly minimum plus $50-200 per contract

- Required for: Buyers trading 10+ contracts monthly (roughly 1+ million gloves monthly consumption)

Executing OTC swaps or structured products

- Investment banks and commodity trading firms act as counterparties

- They customize contract terms to match your specific needs

- They provide credit lines for larger positions

- Cost: Bid-ask spread (typically 1-3% of contract value) plus credit charges

- Required for: Large buyers with $500,000+ monthly raw material spend

When you don’t need a broker:

Fixed-price supplier agreements Your glove supplier or distributor handles all commodity risk management and builds costs into pricing. You simply negotiate contract terms and pricing formulas. This is the most common approach for buyers under 500,000 gloves monthly.

Strategic inventory management Buying extra physical inventory when prices are low requires no broker—just working capital and storage capacity. This “physical hedge” is accessible to all buyer sizes.

Index-linked pricing contracts Negotiating contracts where prices adjust based on published indices requires no broker, just contract negotiation skills.

Choosing the right broker (if needed):

Full-service commodity brokers:

- Provide research, advice, and active management

- Cost: Higher commissions ($100-200 per contract) plus advisory fees

- Best for: Buyers new to hedging who need education and guidance

- Examples: ADM Investor Services, StoneX, Marex

Discount commodity brokers:

- Execution-only service with minimal advice

- Cost: Lower commissions ($50-100 per contract)

- Best for: Experienced buyers who know what they want

- Examples: Interactive Brokers, TD Ameritrade Futures

Commodity trading advisors (CTAs):

- Manage hedging programs on your behalf

- Cost: 1-2% of hedged value annually plus performance fees

- Best for: Large buyers who want outsourced hedge management

- Requires: Minimum $1-5 million in hedging volume

Questions to ask potential brokers:

- What is your minimum account size and monthly activity requirement?

- What are your commission rates and margin requirements?

- Do you provide research and hedging recommendations?

- What is your experience with petrochemical hedging specifically?

- Can you provide references from similar-sized buyers?

- What technology platforms do you offer for monitoring positions?

Alternative to direct broker relationships:

Many mid-size buyers work with commodity consultants who provide hedging advice and strategy but execute trades through the buyer’s own broker account. This separates advice from execution and can reduce conflicts of interest.

Recommended approach by buyer size:

- Under 200,000 gloves monthly: No broker needed—use fixed-price supplier agreements

- 200,000-500,000 monthly: Consider commodity consultant for strategy, use supplier agreements for execution

- 500,000-2,000,000 monthly: Full-service broker for education and execution

- Over 2,000,000 monthly: Discount broker for execution + internal expertise or CTA for strategy

Most buyers should start with supplier-managed hedging and only move to direct commodity trading once volumes exceed 1 million gloves monthly and they’ve developed internal expertise.

What Percentage of My Nitrile Glove Material Should I Hedge

You should hedge 40-70% of your expected nitrile glove material needs, with 50-60% being optimal for most buyers. This partial hedging approach provides meaningful protection against price spikes while preserving flexibility to benefit from price decreases and adjust for demand changes.

Optimal hedge ratios by business profile:

Conservative approach (60-70% hedged):

- You operate on thin margins (under 10%)

- You have long-term fixed-price contracts with customers

- Your demand is highly predictable (less than 15% variance)

- You prioritize budget certainty over potential savings

- Your business can’t quickly pass through cost increases

Balanced approach (50-60% hedged) – RECOMMENDED:

- You have moderate margins (10-20%)

- You have mix of fixed and flexible pricing with customers

- Your demand has normal variability (15-25% variance)

- You want protection with some upside flexibility

- This is the most common approach among experienced buyers

Aggressive approach (30-40% hedged):

- You have strong margins (over 20%)

- You have pass-through pricing clauses with most customers

- Your demand is variable or growing rapidly

- You have strong working capital to absorb price swings

- You want maximum flexibility to capture spot market savings

Minimal hedging (0-20% hedged):

- You operate purely on spot market pricing

- Your customers accept price adjustments

- You have very small volumes where hedging costs exceed benefits

- You maintain high inventory buffers as physical hedge

Factors that increase optimal hedge ratio:

- Longer customer contract commitments (12+ months)

- Thinner profit margins (under 10%)

- Higher price volatility (30%+ annual swings)

- Weaker balance sheet or credit constraints

- More predictable demand patterns

- Rising price trends or supply concerns

Factors that decrease optimal hedge ratio:

- Shorter contract periods (under 6 months)

- Stronger margins (over 20%)

- Lower price volatility (under 15% annual swings)

- Strong working capital and financial flexibility

- Variable or uncertain demand

- Falling price trends or oversupply conditions

Dynamic hedging strategy:

Adjust your hedge ratio based on market conditions rather than maintaining a fixed percentage:

- When prices are in bottom 30% of 5-year range: Hedge 60-70% (lock in favorable costs)

- When prices are in middle 40% of range: Hedge 50-60% (balanced approach)

- When prices are in top 30% of range: Hedge 30-40% (preserve flexibility for price declines)

Calculation example:

A distributor expects to purchase 800,000 nitrile gloves monthly for the next 12 months (9.6 million total). At 4.5 kg synthetic rubber per 1,000 gloves, that’s 43,200 kg or 43.2 metric tons of raw material equivalent.

- Conservative hedge (60%): 26 metric tons

- Balanced hedge (50%): 22 metric tons

- Aggressive hedge (40%): 17 metric tons

They choose the balanced approach, hedging 22 metric tons through a combination of 6-month fixed-price supplier agreement (15 MT) and 6-month crude oil futures as proxy (7 MT).

Common mistakes:

Over-hedging (80-100%): Leaves no flexibility for demand changes or price decreases. If consumption drops 20% or prices fall 30%, you’re stuck with speculative positions that generate losses without offsetting physical savings.

Under-hedging (0-20%): Provides minimal protection. A 40% price spike still causes 32-40% cost increase, potentially wiping out margins on fixed-price contracts.

Static hedging: Maintaining the same hedge ratio regardless of market conditions. Successful buyers adjust ratios based on price levels, volatility, and business conditions.

Recommended starting point: If you’re new to hedging, start with 40% of minimum expected consumption (not optimistic forecasts) for 6 months. Monitor results for two quarters, then adjust based on actual consumption patterns and price movements. Most buyers converge on 50-60% hedge ratios after 12-18 months of experience.

Understanding the composition of nitrile gloves helps buyers calculate precise raw material exposure and determine appropriate hedge volumes based on their specific glove specifications and quality requirements.

Frequently Asked Questions

How much does it cost to hedge nitrile glove raw materials?

Hedging costs typically range from 2-5% of the contract value for fixed-price supplier agreements, 1-3% for direct futures trading (commissions and spreads), and 3-8% for options contracts (premium paid upfront). For a buyer with $200,000 monthly raw material exposure, expect $4,000-10,000 annually in hedging costs depending on the approach used.

Can small buyers with limited volumes still hedge effectively?

Yes, small buyers can hedge effectively through fixed-price supplier agreements rather than direct commodity trading. Suppliers bundle hedging into their pricing, making it accessible to buyers purchasing as few as 50,000-100,000 gloves monthly. Direct futures trading becomes practical only above 500,000 gloves monthly due to minimum contract sizes and transaction costs.

What happens if I hedge and then my demand drops significantly?

If demand drops significantly after hedging, you’re left with excess hedge positions that become speculative rather than protective. This is why experienced buyers hedge only 40-60% of expected needs and base hedges on minimum forecasts rather than optimistic projections. You can close positions early by selling futures contracts or negotiating reduced volumes with suppliers, though this may involve losses if prices have moved against you.

How do I know if my hedge is working effectively?

Measure hedge effectiveness by comparing your actual blended cost (hedged portion plus spot purchases) against what you would have paid buying everything on the spot market. A successful hedge should keep your costs within 10-15% of your target budget regardless of market volatility. Track monthly: hedge position gains/losses, physical purchase costs, blended average cost, and variance from budget.

Should I hedge if I expect prices to decrease?

If you strongly expect prices to decrease, reduce your hedge ratio to 30-40% rather than eliminating hedging entirely. This preserves some protection against being wrong while allowing you to capture most of the expected savings. Remember that hedging is insurance against unexpected increases, not speculation on price direction. Many buyers who skipped hedging because they expected decreases were caught by surprise spikes.

What is basis risk and why does it matter for nitrile glove hedging?

Basis risk is the risk that your hedge instrument (like crude oil futures) doesn’t move in perfect correlation with your actual costs (butadiene prices from your supplier). If crude oil rises 20% but your supplier’s butadiene prices rise 35% due to regional supply issues, your hedge only covers 20% of the increase, leaving 15% unprotected. Minimize basis risk by using hedges that closely match your supplier’s pricing formula.

How often should I review and adjust my hedging strategy?

Review hedge positions monthly to track performance against physical consumption and market conditions. Adjust your overall hedging strategy quarterly based on demand forecasts, price trends, and business conditions. Major strategy changes (like shifting from 50% to 70% hedge ratio) should happen only 2-3 times annually based on significant changes in business conditions or market structure.

Can I hedge other nitrile glove costs besides raw materials?

Yes, you can hedge energy costs (natural gas, electricity) if your supplier passes through energy surcharges, and freight costs through diesel fuel futures if logistics represent a significant cost component. However, raw materials (60-70% of total cost) offer the most meaningful hedging opportunity. Focus hedging efforts where you have the largest exposure and clearest price risk.

What credit or financial requirements do I need to start hedging?

For fixed-price supplier agreements, you need normal trade credit (typically 30-60 day payment terms). For direct futures trading, you need a commodity trading account with 5-15% of contract value as initial margin (cash or securities), plus additional working capital to meet potential margin calls. For OTC swaps, you need established banking relationships and credit lines. Most small to mid-size buyers can start with supplier agreements that require no additional financial capacity beyond normal trade credit.

How do I explain hedging losses to management or investors?

Frame hedging as insurance, not profit generation. When hedge positions lose money because prices fell, emphasize that you achieved the goal of cost certainty and protection against the opposite scenario (prices rising). Show the blended cost (hedge losses plus spot savings) compared to your original budget target. Successful hedging means staying within budget range, not making money on hedge positions. Document hedge rationale upfront so stakeholders understand the strategy before results are known.

Should I hedge in US dollars or local currency?

Hedge in the currency that matches your actual purchase obligations. If you buy from suppliers who invoice in US dollars, hedge in dollars. If you buy in euros or yuan, hedge in those currencies or add currency hedging to your program. Mismatched currency exposure can create additional risk if exchange rates move significantly. Many international buyers hedge both commodity prices and currency exposure separately.

What are the tax implications of hedging gains and losses?

Hedging gains and losses are typically treated as ordinary business income/expenses rather than capital gains, but tax treatment varies by jurisdiction and hedge accounting methods. Consult with a tax advisor to ensure proper documentation and accounting treatment. In many jurisdictions, hedges that qualify for “hedge accounting” treatment allow you to match hedge gains/losses with the physical transactions they protect, smoothing income recognition.

Conclusion

Synthetic rubber price hedging for nitrile glove buyers provides essential protection against the 30-50% price swings that characterize butadiene and acrylonitrile markets. By hedging 40-70% of expected raw material needs through fixed-price supplier agreements, futures contracts, or strategic inventory management, buyers can stabilize costs, protect margins, and bid confidently on long-term contracts despite commodity volatility.

The most successful hedging programs share common characteristics: they hedge partial volumes (50-60%) rather than 100%, match hedge duration to actual contract commitments (6-12 months), use multiple instruments to balance cost and flexibility, and maintain discipline through market cycles rather than reacting emotionally to recent price movements.

For small buyers under 200,000 gloves monthly, fixed-price supplier agreements offer the most practical path to price stability without the complexity and cost of direct commodity trading. Mid-size buyers (200,000-1,000,000 monthly) benefit from hybrid approaches combining supplier agreements with selective futures positions. Large buyers above 1 million gloves monthly should develop comprehensive hedging programs using futures, options, and swaps for precision risk management.

Actionable next steps:

- Calculate your monthly raw material exposure in metric tons based on current and projected glove consumption

- Request fixed-price quotes from 3-5 suppliers for 6-12 month contracts to establish baseline hedging costs

- Analyze historical price volatility for butadiene and crude oil over the past 3-5 years to understand your risk exposure

- Determine your optimal hedge ratio (40-70%) based on margin structure, contract commitments, and risk tolerance

- If volumes exceed 500,000 gloves monthly, interview 2-3 commodity brokers to understand direct hedging options and costs

- Implement a pilot program hedging 30-40% of needs for 6 months to gain experience before expanding

- Establish monthly review processes to track hedge performance against physical costs and budget targets

- Document hedge rationale, entry prices, and target outcomes to enable learning and strategy refinement

The goal of hedging is not to eliminate all price risk or profit from market timing, but to achieve cost predictability that enables confident business planning and protects margins during inevitable supply shocks. Start with modest hedge ratios, gain experience, and adjust based on your specific business needs and market conditions. The buyers who navigate commodity volatility most successfully are those who implement disciplined, consistent hedging programs rather than reacting to each price swing.

For buyers interested in understanding more about the materials and properties that drive nitrile glove costs, explore resources on nitrile glove composition and what to consider when choosing nitrile gloves to make more informed procurement decisions.

SEO Meta Title: Synthetic Rubber Hedging for Nitrile Glove Buyers Guide